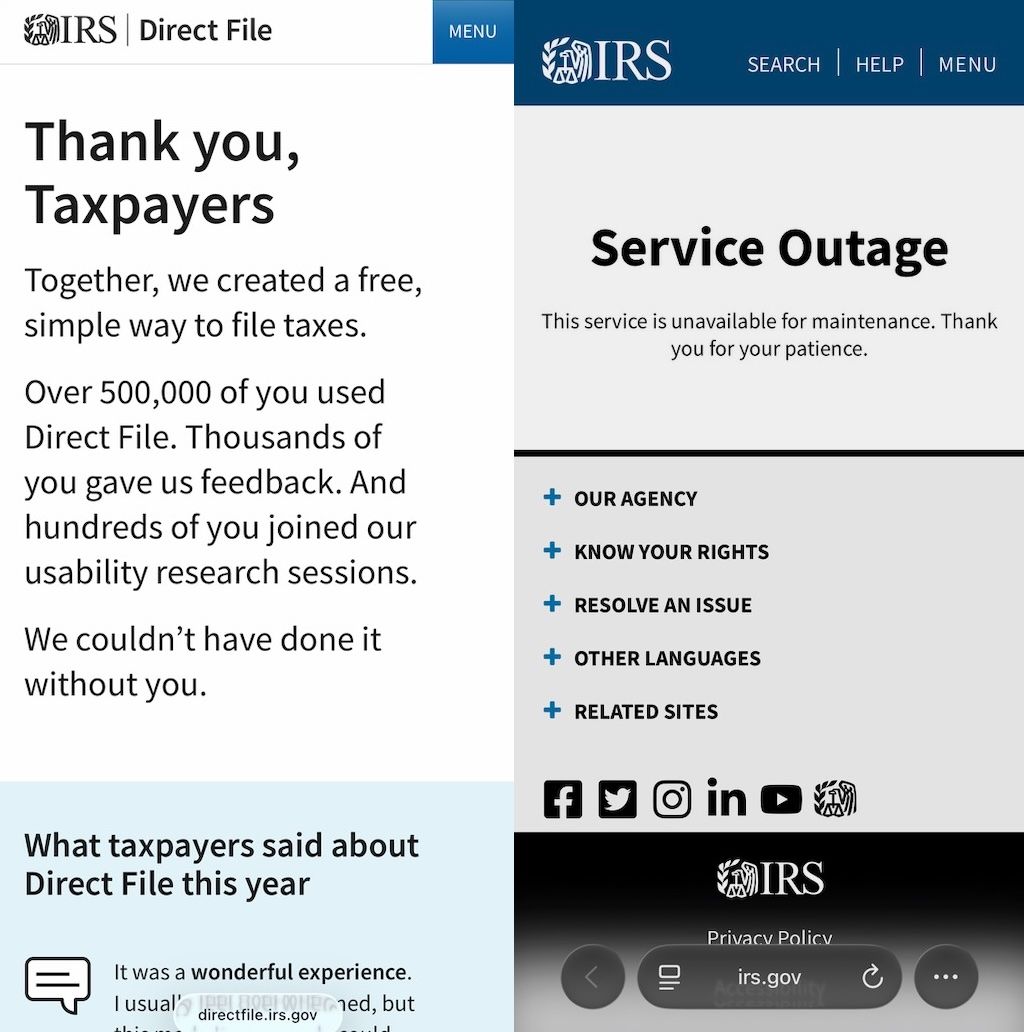

Direct File went live on January 29, 2024. It went dark on November 5, 2025.

Left: Direct File as of November 4, 2025. Right: Direct File today.

The IRS is apparently tearing up its commitment that taxpayers would be able to access their data for three years. Now taxpayers’ only options are to access a transcript online (basically a printout from the IRS mainframe) or to file Form 4506 and pay the IRS $30 to recreate a paper version of their return.

So that sucks. But I do want to memorialize the message that adorned the Direct File homepage for its final two weeks, ever since filing season ended:

Thank you, taxpayers.

Together, we created a free, simple way to file taxes.

Over 500,000 of you used Direct File. Thousands of you gave us feedback. And hundreds of you joined our usability research sessions.

I recently accepted the position of Deputy Secretary for Technology and Innovation of the California Government Operations Agency. I also left DC and moved to Sacramento, driving across the country in my tiny car.[1]

Photo: The southern Rockies come into view on Route 160 in Colorado.

I’ve often given the following advice to technologists who have been bitten by the public service bug at the federal level: find an opportunity to try working for a state or local government. The federal government has incredible advantages. With massive scale comes massive impact from the smallest of things; I sometimes describe the time I wrote a single SQL query that resulted in a couple hundred Veterans’ families receiving quite substantial checks in the mail. And it’s relatively straightforward to pull together a few million dollars for a project in an environment where such amounts are referred to as “budget dust.”

On the other hand, you are often operating at a great remove from the people you serve. I recall an early dissociative experience at VA where I marveled at how the meeting I was participating in, about the business rules for tasks known as “end products” or “EPs,” the types of which were designated by three-digit codes, would have sounded like impenetrable gibberish to an ordinary observer. Bureaucracies are riddled with such abstractions that belie their tangible impact on human life. I think this is a reason there is such power in human-centered design practices, which have the side benefit of cutting through this abstraction and forcing you to confront the ramifications for the everyday experience of services.

At the state and local level, you’re simply that much closer to people. Working at the Office of Early Childhood in Connecticut, I had a modestly sized spreadsheet of every single publicly subsidized child care provider in the state. The task of knowing each and every one of them, and of building relationships with the incredibly devoted people who run them, is eminently within reach. On the other hand, it can be a herculean task to scrape together enough dollars to try out a new approach (even before the federal government’s recent cuts to critical state services like food stamps and Medicaid). At the state and especially at the local level, you just have to be that much scrappier.

California might just defy this axiom. With nearly 40 million people, and an economy that if ranked among countries would be the fourth largest in the world (a factoid frequently noted in conversations about my potential role), California is operating at a scale unlike any other state. Getting to know its government, and its approach to technology, will be an entirely new experience for me. But with federal technology now in the hands of self-absorbed failboy fascists, it tickles me to find refuge advancing progress at the next closest thing.

Photo: The Golden Chain Highway winds through the foothills of the Sierra Nevada, approaching the California Central Valley.

As is already evident, being back inside government will probably stunt any aspirations I may have held of becoming a more regular correspondent. But I still hope to post personal reflections from time to time. If you’re interested in knowing when I do, that’s a great reason to have an RSS reader; the year is 2025, and RSS remains a bright spot in a dark Internet.

A red Chevy Spark, it looks approximately like Apple’s version of the automobile emoji. 🚗 ↩︎

With the federal government abandoning Direct File for now, many state leaders are, admirably, looking for ways to keep the party going. But as the field works to advance the cause of equitable tax system access, it’s important to remember that our goal isn’t just to keep Direct Filing. Our goal is to keep making the sort of transformative progress that Direct File showed was possible: delighted taxpayers, increased trust in government, efficiencies and cost savings, and improved access to tax credits for those who need them the most. In order to get these results without the IRS, states should look to replicate the mindset that brought Direct File to life, rather than simply looking to replicate Direct File itself.

Meeting this moment requires imagination, and as with Direct File, the courage to try something new. We believe this is a time for experimentation and innovation, and states can prove out ideas that the IRS could someday adopt and scale. And there are opportunities to improve state-specific processes and experiences, entirely independent of what the future holds for federal tax administration.

We’ll illustrate this mindset with three examples of experiences that states could create today. These ideas all leverage the unique position of states to craft moments of “wow” for taxpayers, and they could pave the way for Direct File to return better than ever. But these are just a few ideas. An empowered product team working closely with taxpayers, like the teams that designed and built Direct File, could invent many more ideas and far exceed our limited imagination.

I’ve been deliberately steering clear of using this space to react to current events. My last few months in government were discombobulating and highly reactive, and I’ve been trying to get enough distance to be able to think again. So although I’m doing plenty of raging against the calamities of the present moment, I’m not in a place to channel that rage into writing anything of use.

However, I have accumulated a small set of “thing bad” IRS topics that are maybe worth putting down on paper, if for no other reason than to get them out of my brain.

Clue: Direct File Edition

Newly minted IRS Commissioner Billy Long made some off-the-cuff remarks at a conference for tax practitioners, and this kicked off, by my count, the fourth news cycle this year about the killing of Direct File. Don’t get me wrong, as someone who’s emotionally invested in Direct File, jacking into a feed of social media outrage on a regular basis is plenty cathartic in a probably-not-healthy way. And each time the news breaks, word reaches more newly outraged folks. But this is starting to get a little repetitive as someone who has a Google News alert set for Direct File.

It does point to a likely answer for one outstanding question: who’s going to be the one holding the knife? Both Secretary Bessent and DOGE sought to avoid getting their fingerprints on the decision. It looked like Plan A was for Congress to diffusely take the blame, but language terminating Direct File was stripped from OBBBA for parliamentary reasons. They’re currently trying again via a rider on next year’s IRS budget; it’d be nifty if an amendment to remove that provision got a vote and forced members to go on the record. But absent Congressional action, it looks like “Big Beautiful Billy” (his words) will be the fall guy.

OBBBA also included a new $15 million report requiring the IRS to propose a new “public-private partnership” to replace Direct File. I’d wager this presages the triumphant return of Intuit to the Free File game, giving them a chance to recover their past fumbles. I’m also watching for what happens to the $15 million. There’s no conceivable way to spend that amount of money on writing a report in 90 days (let alone a report whose conclusions are already specified by the legislation), so the best possible outcome is the money just doesn’t get spent. The worst outcome is that the administration awards a sweetheart sole-source procurement and wildly overpays someone for little real work.

As for Direct File itself, you can still use it to file your taxes if you haven’t filed yet or requested an extension. Direct File returns are processed the exact same way as any other return, so it’s perfectly safe to use. It’s not dead yet. (But it will most definitely be dead before next year.)

Everyone Saw This Coming

The IRS lives and dies by the filing season calendar, so the comment from the Commissioner that I was most struck by was not his dismissal of Direct File but rather a revealing statement he made about the IRS’s readiness for next year. While nominally projecting confidence about the state of preparations, he warned that filing season won’t start until mid-February, as compared to the usual January timeframe.

It’s only August, and if the IRS is already expecting to be late, things could get much worse before next year. The IRS doesn’t issue refunds until filing season opens, so taxpayers will be angered by not being able to get their money. Even if the schedule doesn’t slip further, with the IRS’s back against the wall, they could be under immense pressure to start filing season before their systems are truly ready, which could result in errors and further delays for some taxpayers.

All of this is the obvious consequence of cutting 25% of IRS employees right before passing a complex new tax law. Even worse than the topline numbers, the “put them in trauma” strategy drove out many of the IRS’s long-time MVPs, the folks who could be counted on to make it work year after year, come hell or high water. Some really great people are still there, but they’re now spread even more thin. I’m rooting for them, but I don’t envy their task.

The IRS knows how bad things could get. I was surprised when the administration appeared to reverse course on its hiring freeze, and posted job announcements for permanent customer support representatives, the folks who field taxpayer questions via phone. But those announcements were quickly canceled without explanation.

Salting the Earth

I’ve been following the administration’s efforts to extract IRS data for use by ICE. Even if the scheme isn’t illegal outright, it seems ripe for abuse.

Every IRS employee is drilled on the importance of protecting taxpayer data. The number 6103, the section of the Internal Revenue Code governing when and how the IRS can share data, is so well-known that it becomes a sort of shorthand, e.g. “I think that’s a 6103 issue.” The collective responsibility to respect taxpayer privacy is such a pervasive cultural ethos, it wasn’t remotely surprising that the Littlejohn data breach was the work of a contractor, not an employee. Stating the obvious, these are not values ICE employees share.

The thing I keep returning to is that, as a means of achieving its stated purpose, I don’t think the data sharing arrangement as it’s currently described will be all that effective. Maybe this isn’t understood by the folks in charge, a result of everyone with an ounce of professional ethics or legal self-preservation staying well clear of the project (or, you know, getting fired). But perhaps there’s another purpose that’s going unsaid.

I think the potential “value” of the effort is the deliberate destruction of trust in government, particularly among immigrant communities, the equivalent of salting the earth after conquest so nothing will grow again. Yeah, that will be effective. To recover from this destruction and someday recultivate trust, it won’t be sufficient to say, “Don’t worry, we’re running things now.”

We’ll need to rebuild in such a way that this isn’t possible. We need to protect privacy with more than just norms and good intentions. And, contra a lot of civic tech orthodoxy, that could mean more restrictions around data sharing, not less.

Judge Carlton Reeves of the Southern District of Mississippi has written some real bangers in his career, but his magnum opus might be his 2018 opinion in Boatner v. Berryhill, an appeal of the Social Security Administration’s denial of disability benefits for a Mississippi man named Carl Boatner. Judge Reeves finds that Social Security wrongly denied Boatner’s claim.

The 26 page decision spends most of its ink reviewing, step by step, why it took the better part of a decade for Boatner to receive the benefits to which he is entitled. This recitation is exhaustive but also breathtaking in its clarity. Headings like “Did Boatner’s ALJ Review the Evidence Properly?” are followed by single-word paragraphs: “No.”

Reeves paints a damning picture of what happens when an administrative process is deprived of the resources to fairly evaluate cases like Boatner’s. He concludes, “Doing justice means finding truth. Finding truth takes empathy, expertise, and time. Without those resources, people who decide disability cases are doomed to do injustice.”

It’s worth reading in full. But the introduction is perfection in its plain acknowledgement of the facts of Boatner’s life and in its determination to not waste a second more of his time.

Carl Boatner spends much of his life waiting. He waits to catch his breath after walking a few dozen steps. He waits for family and friends to assist him in shaving and taking medications. He waits on car rides in rural Mississippi to his many doctor’s appointments. He waits in parking lots while others shop for him, afraid of having a medical emergency in public.

Boatner’s diagnoses include coronary artery disease, two liver diseases, diabetes, obesity, hypertension, spine disorders, major depressive disorder, and anxiety disorder. In 2015, Boatner received a terminal diagnosis of chronic obstructive pulmonary disease, but survived a months-long stay in hospice care.

Even before entering hospice care, doctors described Boatner as “chronically ill” and “disabled.” Between 2011 and 2015, they prescribed him about 17,000 pills. Boatner, now 52, uses oxygen tanks and other devices to help him breathe. He has had a number of strokes and heart attacks, with stents across his heart and liver, and recently had triple-bypass heart surgery. Around 2000, a heart attack ended his two-decade long career as a truck driver. He has not had a steady job since. Boatner last applied for a job in 2015 as a yard hand, but was rejected because the employer thought he “couldn’t hold up.”

Boatner has spent nearly a decade seeking disability payments from the Social Security Administration, filing his last application in 2014. Despite acknowledging the severity of Boatner’s medical conditions and his trips to death’s doorstep, the Administration has denied each of his four applications. These denials have been painful. One caused Boatner to walk out of his house, put a gun to his head, and threaten to kill himself.

Boatner filed this lawsuit to challenge the latest denial. No lengthy judicial opinion need resolve that challenge. Boatner plainly qualifies for disability payments.

But Boatner’s story is worth telling in full. It reveals a disability payment system tasked with managing millions of cases each year, yet stripped of the resources to decide those cases fairly. As Justice Thurgood Marshall once wrote, such an “unnecessary barrie[r]” to people with disabilities “stymie[s] recognition of [their] dignity and individuality,” and therefore requires careful review. Furthermore, the disability payment system aims to be “as protective of people’s dignity as possible,” a purpose “courts must give ‘due regard for.’” The Court must explore why, until today, the disability payment system has left Boatner waiting.

Government writing is usually stripped of all personality, so I like it when civil servants let loose in times of stress. It shows that the faceless bureaucracy is just people trying their best.

Here’s how Social Security’s Lancaster, California district office described the disastrous launch of the Supplemental Security Income (SSI) program on January 1, 1974, in an official report to Washington.

By mid-February we tried “Dial a Prayer,” and by mid-March were negotiating for an exorcist.

Quoted in Martha Derthick, Agency Under Stress: The Social Security Administration in American Government (Brookings Institution, 1990), 26.

Direct File was an obvious idea. Many people had tried to make it happen. The Direct File team was good, but we weren’t any smarter than those who came before. So what made this time different?

I’ve always found Reinhold Niebuhr’s serenity prayer to be a useful thought technology for life in government.

God, give us grace to accept with serenity the things that cannot be changed, courage to change the things that should be changed, and the wisdom to distinguish the one from the other.

Success as a civil servant requires an ample helping of all three traits, particularly serenity. However, “the things that cannot be changed” is not a static category, and it rewards assiduous attention. The smallest shift can make what was once an impossibility suddenly possible.

Direct File had long been on my dream project list, but when I began working on taxes in January 2021, my strong assumption was that any attempt to make it a reality, like those before, would doubtless fail. However, a little failure from time to time is healthy, and I figured it would at least make for a good story someday.

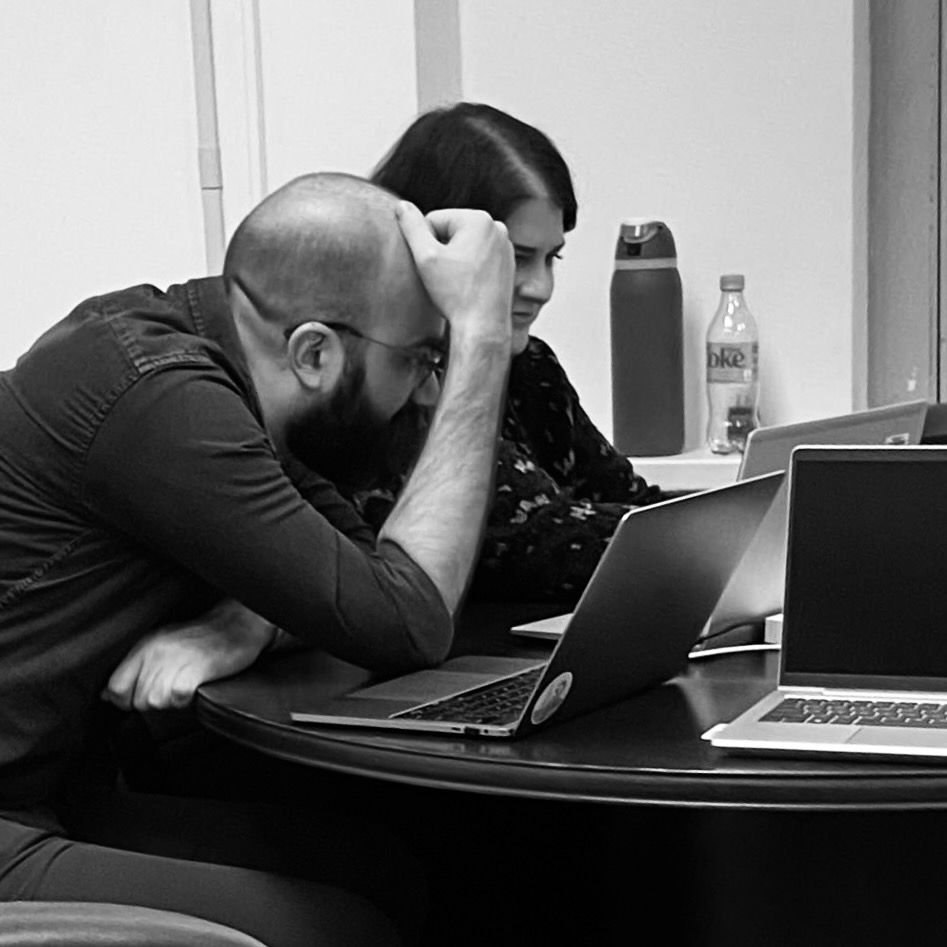

After years of jogging items up and down on my mental list of the most likely ways Direct File would fail, I didn’t realize how thoroughly I had internalized this assumption of doom until the moment Dixie Warden filed the first Direct File return on February 1, 2024. She had agreed to allow Bridget Roberts, Jen Thomas, and me to observe her progress through the application. Direct File still had some significant known bugs, so my responsibility was to call the whole thing off if Dixie ventured too close to certain tax landmines. As she signed and submitted her return, I realized that I had not let myself believe until that precise moment that we would ever actually be allowed to file someone’s taxes.

Photo: Bridget and I watch as Dixie files her taxes, February 1, 2024.

Three years earlier, no one could have anticipated that moment would come. Direct File wasn’t on the agenda. There wasn’t and would never be a grand strategy to mastermind events to bring it about. But events, as is their wont, happened anyway. It’s a stretch to call it “wisdom,” but by setting up at the right place at the right time, we were able to perceive that a window of opportunity had cracked open. These are the three events that made this time different.

1. The pandemic

On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security (CARES) Act was signed into law. One of its provisions was the Recovery Rebate Credit (RRC), more commonly known as stimulus checks, advanced in the form of $1,200 economic impact payments to individuals (plus $500 for each qualifying child dependent). RRC had a subtle but significant difference as compared to a previous programs like that of the Economic Stimulus Act of 2008 (ESA). ESA also provided relief payments to individuals, but it crucially required at least $3,000 of income to qualify for the credit. In the CARES Act formulation, RRC could be claimed by anyone with a Social Security number, even if they didn’t have a cent of income.

The IRS launched a massive effort to get checks out to as many people as possible, working with the Social Security Administration and the Department of Veterans Affairs to identify recipients of Social Security benefits, Supplemental Security Income recipients, and disabled veterans to whom checks could automatically be sent, despite the recipient not having filed a tax return. I’m still astounded and endlessly impressed that the IRS and partner agencies were able to pull off this feat with workforces still reeling from the early weeks of the pandemic.

For everyone else, you needed to have filed a recent tax return in order for the IRS to know how to get you your money. But a small group of federal employees at the Department of Treasury masterminded an ingenious policy hack and issued Revenue Procedure 2020-28, which created a new option for anyone who wasn’t required to file a tax return, generally because they made less than $12,200 or $24,400 for a married couple. Instead of needing to assemble the documentation required to file a full return, these taxpayers could instead file a simplified return claiming just $1 of income.[1] The IRS would understand these to be returns for the sole purpose of receiving an economic impact payment and agreed not to challenge their accuracy.

In order to make it possible to file such a return, Intuit, under the auspices of the Free File Alliance, repurposed the existing Free File Fillable Forms product to stand up a non-filer portal (officially, the “Non-Filers: Enter Payment Info Here” tool). Launched on April 10, just two weeks after enactment of the CARES Act, the non-filer portal enabled millions of additional Americans to receive stimulus checks. An Intuit employee would later describe this work as the most rewarding of his career.[2]

The following year, the American Rescue Plan Act built on the CARES Act model in its expansion of the Child Tax Credit (CTC). The refundable portion of the credit had previously required at least $2,500 of income, but now, in addition to the full credit being refundable, any taxpayer could claim the credit even if they had no taxable income. Hundreds of thousands of kids who had previously been excluded from the benefits of CTC would now see their share of the money.

In order to reach the children of non-filers, the IRS and Treasury dusted off their CARES Act playbook, and on June 14, 2021, they reopened the non-filer portal.[3] But after a year, the portal was seen in a new light. For those who have not had the pleasure of using Free File Fillable Forms, it’s a deliberately excruciating experience.[4] The interface imitates paper forms (don’t try it on a phone) and invites the user to manually type numbers into boxes. The non-filer portal used the same building blocks, so the experience is comparable, just with fewer boxes to type in. That might have been fine for something shipped in two weeks, but there had now been ample time to make it even slightly better.

Congress and advocates began to ask reasonable questions. Can we make this work on phones? Can we get this in Spanish? Can we make it not look sketchy as shit? (Okay, that last one might have just been me.) The IRS’s answer, or what was really the Free File Alliance’s answer: no. Congress didn’t love that answer; neither did the advocates. It’s not a great feeling to go through the rigamarole of passing a law, only for its benefits to not reach those who need them the most because the delivery mechanism is hostage to the whims of a third party incentivized to make that experience as bad as possible. Administration officials were startled to be on the receiving end of this ire.

A senior advisor to Treasury and I had anticipated this eventuality a couple months prior, and we had started a conversation with Code for America about the possibility of them creating an alternative to the official non-filer portal. The result, GetCTC.org, began beta testing in August, and provided the White House with a much needed solution to its portal problem. It worked on phones, its plain language was available in English and Spanish, and for bonus points, it looked like a tool you could trust. The White House enthusiastically promoted GetCTC as part of their CTC outreach efforts.

Even as a nonprofit came to their timely aid, however, officials had learned an object lesson about what it meant for the government to not be in control of its own destiny, a lesson that would not soon be forgotten.

2. Intuit leaves Free File

Those alive at the time will always remember where they were when they heard JFK was shot. I will always remember where I was when I heard Intuit was leaving the Free File Alliance.[5] It was an event that so completely upended what was possible, I was vibrating for a week afterwards.

Free File was created in 2002 and successfully forestalled the development of Direct File by more than twenty years. The Bush Administration had established “E-Government” as a core pillar of its President’s Management Agenda and proposed the creation of “an easy, no-cost option for taxpayers to file their tax return online.” At the time, the average cost of electronic filing via a third party was just $12.50 ($22.41 adjusted for inflation), which the administration noted was quite a bit more than the cost of a 34 cent stamp.[6]

The tax preparation industry scrambled for an alternative. Intuit organized its competitors to form the Free File Alliance and offered the IRS a deal: the companies would agree to provide free versions of their products to low-income Americans in exchange for the IRS committing to not offer online filing. Heralded as a “public-private partnership,” the arrangement appealed to the White House, despite some hesitation from the Office of Management and Budget and Treasury.

For its part, the IRS was relieved to not have to undertake a risky, high-profile IT project. The memory of 1996’s Cyberfile disaster was still relatively fresh. In late 2022, I attended the retirement party of a long-time IRS employee and chatted with someone who was closely involved in the early E-Government work. He recalled of Free File, “We were given just nine months to get something out the door.” He gave me a wry smile. “Sounds familiar, no?” He wished me luck; it was clear he thought Direct File would need it. (He wasn’t wrong.)

What happened next has been well documented, including actions the IRS took to limit the scope of the Free File program out of concern for the “future revenues and profits of the publicly traded company participants,” actions that had Free File taken on its own behalf, would have constituted illegal collusion and price fixing. Apparently by design, Free File usage dwindled.

In 2005, the IRS terminated its TeleFile program, which let taxpayers file via phone.[7] Paper returns were now the only remaining way to file without going through a third party. The success of electronic filing relied on the goodwill of industry. Efforts to prevent identity theft and refund fraud hinged on the voluntary participation of companies, and the IRS was often negotiating from a position of weakness.

Then came 2019, a tumultuous year for Free File. The year started promisingly enough, with the near realization of lobbyists’ long-held dream of enshrining Free File into law via the Taxpayer First Act. However, public backlash resulted in this provision being stripped, and over the coming months, reporters at ProPublica released a series of articles highlighting deceptive industry tactics. Investigations were launched, and by the end of the year, Free File was on its heels. In an attempt to deescalate, Free File and the IRS agreed in December to remove the language from their Memorandum of Understanding (MOU) that barred the IRS from offering Direct File.

Both parties understood that this was for show. Little had changed, and the IRS’s hands remained effectively tied. When I arrived at the agency in 2021, Free File was described to me as “the third rail of the IRS.” Venture too close to that third rail, as the Volunteer Income Tax Assistance program found out when its Facilitated Self Assistance model became too popular during the pandemic, and you could expect to be put on blast by industry lawyers during tense phone calls.

I saw Free File less as a third rail and more as a Gordian Knot. The way it prevented Direct File was not by explicitly barring it, nor via awkward meetings, but rather by making it too hard to do anything else. Despite Free File’s underutilization, there were about four million taxpayers who used it in filing season 2021. Even after the prohibition was dropped in 2019, the MOU still contained the following clause:

Should the IRS commit funding to offer Services for free to taxpayers the IRS shall notify [Free File] immediately. If the IRS gives such notice during the tax season (between January 1 and April 15 […]) of any year, [Free File] may, by written notice to IRS, terminate this MOU, effective on April 16 […]. If the IRS gives such notice between April 16 […] and October 15 of any year, then [Free File] may, by written notice to IRS other than during tax season, terminate this Agreement, such termination to be effective no fewer than 30 days after the date of [Free File]'s notice of such termination. If IRS gives such notice between October 15 and December 31, [Free File] may by written notice immediately terminate this Agreement at any time on or before December 31.

The notification clause allowed industry to take their ball and go home the moment the IRS committed a single dollar to Direct File, instantly depriving some number of taxpayers of the method they used to file. But since the IRS had been sitting on the sidelines for literal decades, it would require years of work to catch up and create a service that could address the diverse tax situations of all of those taxpayers to the standards of the IRS. In the short-term, some people would need to find a new way to file, and industry would point the finger at the IRS. The IRS had no room to maneuver out of the predicament in which it had been trapped.

Then on July 15, 2021, Intuit announced that it would no longer participate in Free File, following the lead of H&R Block in 2020, leaving only TaxHawk (aka FreeTaxUSA) and a number of smaller companies to man the fort. The eminently predictable result was that a million fewer people used Free File in 2022. How did this enable Direct File?

In short, Intuit gave up its leverage. In the chronology as it played out, there are four events. (1) Intuit announces it’s leaving Free File. (2) A million fewer people use Free File. (3) The IRS announces it will pilot Direct File. (4) 140,803 people use Direct File in a limited pilot.

Now imagine a different chronology. (1) The IRS announces it will pilot Direct File. (2) In response, Intuit announces it’s leaving Free File. (3) A million fewer people use Free File, and only 140,803 people use Direct File. I would argue that in this world, Direct File would have been dead on arrival. The IRS would have gone through a whole lot of trouble for the net result of fewer people filing their taxes for free. It just didn’t work politically, and I saw no way of untangling that knot.

But then Intuit cleaved the knot for us. And so when the Direct File pilot happened, Free File saw a significant increase in usage, the result of more taxpayer interest in options for filing for free (and admittedly, a whole lot of Free File/Direct File brand confusion). Taxpayers had more options, not less, and more of them were able to file for free, an unambiguous win.

(Now that Direct File lies comatose, Intuit gets a second bite at the apple, and they and the rest of the tax preparation industry will attempt to restore their leverage over the IRS and state revenue agencies, lobbying legislators and attempting to persuade/bully tax administrators into doing long-term damage to the government’s negotiating position. Something to watch for.)

3. The Inflation Reduction Act

There is a pervasive narrative, supported by many talking points to this effect, that the Inflation Reduction Act (IRA) led to Direct File. And it did, but maybe not in the way you think. The IRA’s impact wasn’t just money, or a report; it completely inverted the political calculus around Direct File.

Certainly the IRA’s $80 billion in IRS funding provided ample elbow room for new initiatives like Direct File, and I never again had to answer the question, “But where will the money come from?” However, over the entirety of my time on the project, the IRS spent on Direct File an amount less than 0.1% of the funding provided by the IRA. As a share of the IRS’s scant enacted budget excluding IRA funds, Direct File would have comprised 0.26%, the equivalent of an ad-free Netflix subscription for a household earning $80,000. The IRA funds put wind in our sails, but Direct File was never going to break the bank.

The IRA contained a provision asking the IRS to spend $15 million to write a report about Direct File. After delivery of the report, the Secretary of the Treasury directed the IRS to pilot Direct File in filing season 2024, and the rest is history. But as the author of multiple sections of that report (full credit to Amy Paris as the primary author; she would agree), there’s no way our words alone would have been worth $15 million, particularly compared to the $24.6 million price tag of producing a report and shipping the damn thing (and producing a second report as a bonus). There’s a case to be made that the report to Congress was politically useful, but I think this case is overstated and relies heavily on post hoc reasoning. I can only hope lawmakers realize before repeating the experiment that despite Direct File’s success, the likeliest outcome of the provision was a costly but swiftly forgotten report. (Oh. Oh no.)

No, the IRA’s greatest contribution to Direct File: it passed.

During the early discussions of Direct File, the greatest reluctance came from a contingent, particularly in Treasury, who believed it would jeopardize the legislative chances of what was then called the Build Back Better Act, and in particular, its banner rejuvenation of the emaciated IRS budget. The Senate was split 50/50, and Democrats only held a technical majority via the tie-breaking vote of the Vice President. Unable to lose even a single vote, the camp resisting Direct File viewed movement on a “controversial” program as the straw that would break the camel from West Virginia’s back.[8]

Even as Build Back Better’s prospects looked increasingly grim, hope sprang eternal on Pennsylvania Avenue,[9] right up until Senator Manchin hammered what appeared to be the final nail in the act’s coffin on July 14, 2022. But less than two weeks later, well before this new reality could sink in, Senators Manchin and Schumer announced they had struck a secret deal to save the tax and climate portions of the bill, and unveiled the IRA. It swiftly passed and was signed into law on August 16.

Not only was their Direct File hesitance now obviated by the bill passing Congress, the proponents of additional IRS funding faced a new challenge. They needed to demonstrate to the American public the value of investing $80 billion in the IRS. For policy wonks, the case was a slam dunk. The IRA would enable the IRS to pursue high-income individuals and multinational corporations, whose complex returns had escaped scrutiny as the IRS was starved of resources. The Congressional Budget Office estimates that each additional dollar invested in tax enforcement yields between $5 and $9 of additional revenue. More funding for the IRS wasn’t spending money, it was raising money by enforcing the laws already on the books.

But $80 billion is a lot of money, and even the wonks understood that the IRS needed to show taxpayers a tangible return for this massive investment. Answering phones and clearing paper backlogs were obvious and important service wins, but these accomplishments wouldn’t be felt by most taxpayers.

The IRS needed something bigger, something exciting, something that showed that the bar had been raised for the kind of services taxpayers could expect from an adequately funded agency.

Consensus was within reach. Direct File was no longer a thing that couldn’t be changed, and it had quite suddenly become a change that voices across government were clamoring for, if only the IRS could find the courage.

IRS systems didn’t support tax returns with $0 of income, thus the hack of telling everyone to say they made a buck. ↩︎

I say without malice that he should consider public service. ↩︎

The delay until June was to avoid taxpayers choosing simplified filing over filing a full return, which in many cases would allow the taxpayer to claim additional benefits. ↩︎

It’s how I file my own taxes, since DC was waiting until 2026 to join Direct File. I guess I’m going to continue doing so, unless I switch to paper as a small protest against Direct File’s termination. ↩︎

Outside of Ted’s Bulletin on 14th Street Northwest. I had just gotten dinner with friends, one of whom (coincidentally a former Intuit employee) had asked that we stop at Ted’s so she could get a malt. The resulting shake turned out to be mostly malt powder, so she had gone back inside to ask for a more correctly proportioned replacement. While we waited, another friend (actually the senior advisor to Treasury) was checking his phone and announced, “Huh, Intuit’s leaving Free File.” For the record, any amount of malt powder is a fine way to ruin perfectly good ice cream. ↩︎

The E-Government team also recognized the importance of authentication, and they proposed the creation of a single sign-on for government. They warned, “Not undertaking a consolidated authentication approach would cost an additional $200 million in development costs, $26 million in acquisition costs and would delay implementation of the E-Government initiatives to 2005 and beyond.” Oh, if only they knew. ↩︎

One of the engineers who built TeleFile also worked on Direct File, playing a key role in developing the State API, among other contributions. ↩︎

At no point has Direct File actually been controversial; pollingshowsmassivepopularsupport among taxpayers across the political spectrum. The only opposition is from lobbyists. ↩︎

Main Treasury and the White House are next-door neighbors on Pennsylvania Avenue. ↩︎

IRS officials were unable to show us that they had independently documented measurable goals or objectives to manage the outcomes of its identity-proofing program. According to federal internal control standards, officials should define objectives clearly to enable the identification of risks and define risk tolerances. Without independently established measures and goals, IRS cannot determine whether the performance of ID.me’s solutions meets IRS needs.

Without goals or objectives set by IRS, it is also not clear which of the several measures that ID.me provides are the best matches for what IRS needs or what level of performance is appropriate for a given application. For example, ID.me’s true pass rate excludes both users who abandon the process and users identified as highly probable fraudulent. In establishing measurable goals, IRS could determine that information on such users are essential performance measures that need to be established. Furthermore, as IRS continues to expand online services that require identity proofing it will need to consider additional metrics for these services.

At some point I’m going to write a long post about Direct File and identity. Today is not that day. But expect this report to be cited when I do.

GAO reports are pretty technical, and it’s understandable that some of the early takes I’ve seen kind of miss the mark. This is the key point: the IRS abdicated its responsibility to define what good looks like, outsourcing that responsibility to its vendor.

So last week’s post was not so subtly a provocation for the “just add AI” approach to government. But hey, now that I’ve already done the work of sussing out what’s going on and writing it out in detail, let’s add AI and see what happens.

I asked ChatGPT to read the post and suggest a few ways the algorithm could be improved.

Thanks for sharing the post. It’s a rich and thoughtful deep dive into a real-world government algorithm with significant care and attention to fairness, complexity, and transparency. Still, even great systems can be improved. Here are several ways the algorithm might be enhanced or revisited, based on what the blog described.

Oh god, the sycophancy.

Reduce Reliance on Heuristics in Proportional Allocation

Current approach: The AMA algorithm uses fixed parameters like the INTERPOLATED_DIRECT_REVIEW_PROPORTION_ADJUSTMENT (e.g., 67%) and a MAXIMUM_DIRECT_REVIEW_PROPORTION cap (e.g., 80%).

Suggested improvement: Replace static interpolation factors and hardcoded caps with dynamic, data-driven optimization. Techniques like Bayesian updating or reinforcement learning could help the system adapt in real time based on backlog levels, processing rates, and success in meeting deadlines.

Right off the bat, I think this provokes an interesting question. ChatGPT suggests a system that requires less human intervention because it optimizes itself toward a defined set of goals.

In the algorithm as I designed it, there are certainly examples of exactly this. You could imagine a version of the algorithm that preserved the concept of “docket month,” and allowed a human operator to specify how deep on the docket the machine was allowed to look, historically a policy decision that humans at the Board had been making. In this case, I opted to completely replace this process. Given the pace at which humans can orient and act upon new information, a process with a human in the loop would necessarily require a greater margin of error, and it was better for the algorithm to determine the most efficient possible parameter at any given time.

The same could be said for the parameters ChatGPT has called out above. Except that I think those items differ from the docket month example in terms of the pros and cons that must be weighed to change them. There is no right answer to whether the Board should prioritize Direct Reviews over legacy appeals.

These are policy questions in a complex decision space without an optimal answer. As I explained the algorithm to different audiences, one thing that I would always emphasize was that it provided “levers” that decision makers could pull. It wasn’t my place to decide those questions as the algorithm’s designer, as I would if I had obfuscated my opinions via an optimization function specified in a black box algorithm.

Implement Feedback Loops for Goal Reassessment

Current approach: The system assumes the 365-day goal for Direct Review decisions remains static, even when it becomes unrealistic.

Suggested improvement: Introduce a feedback mechanism that automatically flags when a policy goal (like the 365-day target) is routinely being missed, and prompts a reassessment. This could be both internal (staff dashboards, alerts) and external (public transparency reports).

This is right on, and actually prompted me to go back and add a note about the dashboard we built for this very purpose. (ChatGPT read an early draft; I was paranoid it might find some egregious error past me had made and thus undermine current me’s whole reason for writing.) But I like the suggestion that the data should be public.

Address Race Conditions in FIFO Distribution

Current approach: Race conditions can occur when two judges request cases simultaneously and might skip over the true “oldest” FIFO case.

Suggested improvement: Introduce record-level locking or atomic fetch-and-assign mechanisms at the database level, even for legacy VACOLS records, possibly via a transactional wrapper layer or a temporary in-memory locking system.

My post flagged this as a theoretical problem, and yeah, it’s totally fixable. Caseflow already was using Redis; it wouldn’t have been hard to implement a locking mechanism. Heck, I added locking in Redis to my Slackbot to look up acronyms, which was nowhere near as mission critical. But the cost is adding complexity to the system, adding one more thing that could break. Given the negligible potential impact, I think I can defend letting that one go.

Use Better Predictive Models for Case Inflow and Processing Time

Current approach: Direct Review pacesetting proportions and legacy NOD adjustments are based on historical averages (e.g., 40% of NODs becoming Form 9s).

Suggested improvement: Use predictive analytics or machine learning to estimate case inflow and judge workload more precisely. For example:

Train models on NOD metadata to predict Form 9 likelihood.

Use survival analysis to forecast case readiness timelines.

Update predictions continuously based on actual outcomes.

This one’s amusing to me. Once I finally got a VA computer (six weeks after I started work at VA), one of the first things I did was use survival analysis to model the appeals process end-to-end. Those models ended up having a ton of uses, both internal (workforce planning) and external (time estimates for Veterans checking their appeal’s status on VA.gov). ChatGPT would be proud. As for whether I should have plugged those models into the algorithm instead of the hardcoded 40% heuristic, nah, not worth the extra complexity.

More Granular Customization of Batch Sizes

The feature it turned out nobody needed? Yeah, not adding that. I guess I did call it a “disadvantage,” though, so that one’s on me.

Improve Fairness Monitoring Across Judges

Add Resilience for Sudden Capacity Shifts

These are nice sounding words that mean nothing.

Publish Algorithm Documentation and Code

Current approach: The algorithm used to be public but was removed from GitHub.

Suggested improvement: Restore the public repository, redacting any sensitive implementation details, to meet modern expectations for algorithmic transparency in government decision-making. This helps build trust and allows outside experts to contribute improvements.

This is a blog post about designing algorithms for government. “Algorithm,” in this context, just means “an automated way of making a decision.” I am going to describe, in great detail, a specific algorithm that I created for the U.S. Department of Veterans Affairs (VA). If you’re a U.S. Veteran who had an active case with the Board of Veterans Appeals (the Board) at any time since November 2018, this algorithm affected your appeal.

This post is going to get wonky. And it’s very long. I’m going to try my best to inverted pyramid this thing. It’s entirely okay to stop reading when you’ve had enough. There isn’t a twist at the end. There isn’t a reward for having finished it. The only reward is more detail. There is no bottom.

I’m sorry.

Why does any of this matter?

I hope to illustrate three things.

First, this is a story about automation. In this story, I automate a manual, bureaucratic process, from start to finish. But no one was fired, and in fact, the people who used to own the process were thrilled to be able to focus on more important work. To quote Paul Tagliamonte, “Let machines do what machines are good at, let humans do what humans are good at.” Everyone on all sides of this automation story was committed to doing right by Veterans. I sought to approach the task with the same level of care as its former stewards had done for many years, and I leveraged insights from the manual steps they had worked out through trial and error.

Automating this process involved more than just translating legal rules into instructions for a machine. The manual process involved bounded but significant discretion to ensure that the appeals continued to move apace. As we’ll see, a statutory change created even more opportunities for discretion. Machines don’t do discretion (or at least, they shouldn’t). So in concretizing the process into an algorithm, that discretion falls to the algorithm’s designer. Automation is thus a kind of rulemaking, but without established methods of public participation like notice-and-comment. And even while the decision space was sufficiently constrained to preclude bias on the basis of protected factors, I still needed to grapple with fundamental questions of fairness and ensure that humans remained in the driver’s seat.

Second, this is a story about complexity. You hear about civil servants studiously attending to their small niche of bureaucratic arcana, and this is a guided tour of one such niche. It’s not my niche; I was just a visitor. If, a couple thousand words into this post, the fleeting thought “maybe this whole process should just be simpler” crosses your mind, I understand. And maybe it should be! Sometimes complexity is a once good idea that’s gone rotten with time. Sometimes it was always a bad idea. But I guarantee there was intention behind the complexity. It’s trying to help someone who was left behind. It’s there because a court ordered that it must be, or because Congress passed a law. And sometimes, it might actually be load-bearing complexity. Take a sledgehammer to it at your own risk.

I think we should strive to “make it simpler” more often. Certainly I feel that Congress and the courts rarely give the challenges of implementing their will due consideration, nor do they always consider how things like administrative burden can adversely affect outcomes. But from the standpoint of most government workers, you have no choice but to make complexity work every single day. This is a story about how to make it work.

Finally, this is a story about transparency. The system that we are going to be looking at was developed in the open. Anyone in the world could check out its source code or read discussions the team had while designing and building it. This system manages every Veteran’s appeal, and instead of asking them to trust us, we’re showing our work. Because the U.S. government built it, it’s in the public domain, and you can find it on GitHub.

Except that’s a dead link. It’s dead because VA decided to take a project that had successfully operated with complete transparency for more than three years and hide it from the public. I don’t know why they decided to do that; I was long gone. I have no reason to believe there were any nefarious motivations, apart from a desire of certain officials to steer the project in a very different direction than that which my team believed in (a direction that, as the subsequent years have made clear, has not worked out).

So I’m going to have to describe the algorithm as it existed when I left VA in May 2019. I can tell from the Board’s public reports that, at a minimum, the parameters of the algorithm are set to different values than when I left (which is great; that’s why I put them there). Maybe the algorithm itself has been completely replaced (that would be cool; I don’t have a monopoly on how to solve the problem, and maybe I got something wrong!).

What’s not cool is that the public has no way of knowing, that Veterans have no way of knowing. For all I know, the algorithm has been replaced by an octopus (literal or figurative).

It is just a tiny component of a tiny system in a tiny part of VA, which is just one part of the U.S. federal government. But all across government, more and more decisions are being automated every day. For all the attention paid to the introduction of automation into decisions of enormous consequence rife with potential for discrimination (rightly so!), there are a host of smaller decisions that nevertheless matter to someone. How we approach the task of automating these decisions matters. The guardrails we put around it matter. Whether anyone even understands how the decision was made matters.

If you make it to the end of this post (and again, it’s really, really okay if you don’t), you will be able to explain every decision this particular algorithm will ever make. Why shouldn’t every government algorithm be knowable in this way? No, you couldn’t possibly invest the time to understand each and every algorithm that affects your life (are you absolutely sure you want to invest it here?), but wouldn’t it be reassuring to know that you theoretically could? (And, satisfied in the knowledge that you could have read this post to the end, wouldn’t it be so much better to go to your local library and pick up a nice Agatha Christie?)

What it do?

When a Veteran appeals a decision made by VA, such as a denial of a claim for disability benefits, they enter a sometimes years-long, labyrinthine process. Eventually, their case will reach the Board, a group of more than 130 Veterans Law Judges and their teams of attorneys, who decide the appeal.

At time of writing, there are more than 200,000 appeals waiting for a decision from the Board.[1] These appeals wait on a “docket,” which is lawyer speak meaning they wait in a line. Per the regulations, “Except as otherwise provided, each appeal will be decided in the order in which it is entered on the docket to which it is assigned.”[2]

When a judge is ready to decide another appeal, they need to retrieve the first case on the docket, the next case in line. The algorithm we’re discussing determines what case to give the judge. It’s called the Automatic Case Distribution algorithm.

That’s it. Really. “What’s the next case in line?” is all we’re doing here.

Of course, as you scroll through this 6,400 word blog post, you can probably guess that it’s going to get a lot more complicated than your average deli counter. The manual process was run by a team of four people (with other responsibilities too), armed with lots and lots of Excel spreadsheets.

Then Congress passed the Veterans Appeals Improvement and Modernization Act of 2017. Now the Board would have not one, but four dockets. Any chance that four humans could keep track of it all went out the window. Now automation wasn’t optional, it was essential. But before tackling all of that complexity, I started by automating just the one docket. So let’s start there too.

Easy mode: a single docket

When an appeal arrives at the Board, it is assigned a sequential docket number that starts with the date.[3] If we just sort the appeals by that number (and thus, implicitly, by the date they arrived), we’ll get a list of appeals in docket order.

Judges request appeals in batches, which they’ll divvy up among their team of attorneys, who will review the available evidence and write decisions for the judge to review and sign.

In order to supply a judge with a fresh batch of cases, the team managing the docket would run a report in the legacy Veterans Appeals Control and Locator System (VACOLS) to retrieve a spreadsheet of the oldest cases ready to be decided. Working in docket order, they would move the requested number of cases to the judge in VACOLS and email the judge a list of those cases for tracking. (Before the case files were digitized, the paper case file would also need to be sent to the judge’s office.)

It’s pretty easy to imagine what this process looked like once automated. The judge would log into Caseflow, the system we were building to replace VACOLS. Assuming they had already assigned all of their pending cases to attorneys, they would be presented with a button to request a new batch of appeals. Click that and new cases would appear, ready to be assigned.

One downside of the automated approach relative to the manual process was that I designed it to always assign each judge a set number of cases, three cases for each active attorney on the judge’s team. This parameter, cases per attorney, was configurable by the Board, but not by individual judges. Back when the humans were running things, judges were able to request whatever number of cases they wanted. But in user research with judges, we didn’t hear that anyone really needed to customize the number of cases, a finding that was confirmed after we launched and didn’t get any pushback. Using a fixed number of cases, called the batch size, kept things more predictable.

There are two complications we have to care about. First, some cases are prioritized. A case can be prioritized because it is Advanced on the Docket (AOD), a status granted to cases where the Veteran is facing a financial or other hardship, a serious illness, or is 75 years or older. A case can also be prioritized because the Board’s decision was appealed to the Court of Appeals for Veterans Claims (CAVC) and it was remanded back to the board to correct a problem. If the case is prioritized, it must be worked irrespective of docket order.

Second, if a judge had held a hearing with the Veteran, or if they had already issued a decision on the appeal, that appeal is tied to the judge and must be assigned to them, and no one else. If the judge retires, the Veteran would need to be offered another hearing with a different judge before the Board could decide the case.

For these reasons, the humans had a more difficult task than just selecting the first several rows of a spreadsheet. Prioritized cases were front of the line, but they didn’t want any single judge to become a bottleneck after getting assigned too many of the most time-sensitive cases, so the team would try to ensure that each judge got a balanced number of AOD cases, while also ensuring that no AOD case sat too long.

If there were cases that were tied to a particular judge, it wouldn’t make sense to assign that judge a bunch of cases that could have been worked by anybody (gen pop cases). So the team was allowed look past the strictly oldest cases on the docket to keep things moving. In order to keep this aboveboard (after all, cases are supposed to be assigned in docket order), each week the team would determine a “docket month” by calculating the age of the Nth oldest case, where N was a number that was agreed upon by the Board and stakeholders. Any case that was docketed in that month or before was considered fair game, giving the team the wiggle room they needed to keep things moving smoothly.

The algorithm basically replicates this approach, with some machine-like flair. The concept of docket month, an easy-to-use tool for humans to keep track of which cases they could assign, is an unnecessary abstraction for a computer. I replaced it with a concept called docket margin. Even though judges request cases on their own schedules, the algorithm starts by asking, “What if every single judge requested a new batch of cases at the same time? How many cases would I distribute?” That count is our docket margin, a rough estimate of the concurrent bandwidth of the Board.

To determine how many prioritized cases to give to each judge, we count the number of prioritized cases and divide it by the docket margin to arrive at the priority target. Multiplying the batch size by this proportion and always rounding up, we arrive at the target number of prioritized appeals we want to distribute to the judge.

Here’s some Ruby code. The code is just another way of saying the same thing as the above paragraph, so if don’t like to read code, you’re not missing anything.

defpriority_target

proportion =[legacy_priority_count.to_f / docket_margin,1.0].min

(proportion * batch_size).ceil

end

We can also use the docket margin to derive the docket margin net of priority, which is the docket margin minus the count of prioritized cases. Like the docket month, this range determines how far back we are allowed to look on the docket and still be considered to be pulling from the front of the line. Unlike the docket month, it is calculated on demand and is more precise.

defdocket_margin_net_of_priority[docket_margin - legacy_priority_count,0].max

end

Now we have everything we need to distribute cases from our single docket. The algorithm has four steps.

In the first step, we distribute any prioritized appeals that are tied to the judge requesting cases. As no other judge can decide them, we will distribute as many such appeals as we have ready, up to the batch size.

In the second step, we distribute any non-prioritized appeals that are tied to the judge. We will again distribute an unlimited number of such appeals, but only searching within the docket margin net of priority, i.e. the cases that are considered to be at the front of the line.

Note that, in terms of the ordering of the steps, we are considering first whether the appeal is tied to a specific judge before considering whether the appeal is prioritized. This is because at the micro level, it’s more important for any given judge to be working the cases that only they can work. At the macro level, between the Board’s more than 130 judges, there will always be plenty of judges available to work AOD cases quickly. Note that even in extreme circumstances, such as if every appeal was tied to a judge, the algorithm would be self-healing, because the docket margin net of priority shrinks the more prioritized cases are waiting, thus reducing the number of cases distributed in step two.

In the third step, we check the priority target. It’s possible we already hit or even exceeded the target in step one, in which case we skip this step. But if we still need more prioritized cases, we’ll distribute gen pop prioritized cases until we reach the target. In order to ensure that prioritized cases continuously cycle, they are not sorted by docket date, but rather by how long they’ve been waiting for a decision, or in programmer speak, a first-in, first-out (FIFO) queue.

At any point, if we have reached the limit of the batch size, we stop distributing cases. Our work is done.

But assuming we still need more cases, our fourth and final step is to look to non-prioritized, gen pop appeals. We distribute those in docket order, until the we’ve reached the batch size and the judge has the cases they need.

Here’s what it looks like in code:

deflegacy_distribution

rem = batch_size

priority_hearing_appeals =

docket.distribute_priority_appeals(self,genpop:"not_genpop",limit: rem)

rem -= priority_hearing_appeals.count

nonpriority_hearing_appeals =

docket.distribute_nonpriority_appeals(self,genpop:"not_genpop",range: docket_margin_net_of_priority,limit: rem)

rem -= nonpriority_hearing_appeals.count

if priority_hearing_appeals.count < priority_target

priority_rem =[priority_target - priority_hearing_appeals.count, rem].min

priority_nonhearing_appeals =

docket.distribute_priority_appeals(self,genpop:"only_genpop",limit: priority_rem)

rem -= priority_nonhearing_appeals.count

end

nonpriority_appeals =

docket.distribute_nonpriority_appeals(self,limit: rem)[*priority_hearing_appeals,*nonpriority_hearing_appeals,*priority_nonhearing_appeals,*nonpriority_appeals

]end

Congratulations, that’s one full government algorithm. It was turned on in production in November 2018, but it would only stay on for three months…

The Appeals Modernization Act

On August 23, 2017, the Veterans Appeals Improvement and Modernization Act of 2017, a.k.a the Appeals Modernization Act (AMA), was enacted into law. The first significant reform of the VA appeals process in decades, VA was given 540 days to implement the new law. There’s no possible way this already overstuffed post can accommodate my opinions about AMA and how it was implemented, so let’s just narrowly focus on what this new law meant for the Automatic Case Distribution algorithm.

My team was working to replace VACOLS—a legacy system, built in PowerBuilder, that had been maintained for decades by a single person—with Caseflow. The passage of AMA was a clarifying moment for our team. It was quickly apparent that there was no path for VACOLS to be retrofitted for the new law, so the 540-day clock provided a deadline for Caseflow to be able to stand on its own two legs.

545 days later, VA was ready and the law went into effect. Nothing changed for Caseflow. Every single piece of new functionality had already gone live in production and been used to manage the real appeals of real Veterans via the Board Early Applicability of Appeals Modernization (BEAAM) program,[4] which invited a small group of 35 Veterans to conduct a trial run of AMA. The program not only helped to ensure a smooth rollout of the technology, but it also gave us valuable insights as we prepared updated regulations and procedures for the new law and designed informational material for Veterans and their representatives.

By the way, I think this is the Platonic ideal of government IT launches. You just throw a nice party for the team because everything has already shipped.

Photo: And you buy jumbo scissors, February 19, 2019.

Everything had gone live, that is, except for the new version of the Automatic Case Distribution algorithm. The whole reason we implemented the single-docket algorithm described above, despite only needing it for three more months, was so that we could roll out as much as possible ahead of the applicability date of the law. But on AMA day, we had to flip a feature flag and swap in a completely different algorithm.

In order to test the new algorithm ahead of time, I built a discrete-event simulation (DES) to model what the Board would look like under AMA, and I used that to pressure test the algorithm under various conditions. I had done the same for the single-docket version before rolling it out too, although that was easier thanks to decades of historical data. For example, when I said above that docket margin net of priority was “more precise” than docket month, the evidence for that claim before we took the algorithm live was simulation results showing that it never had to look more than 3,000 cases deep on the docket, which was narrower than the range the humans were using at the time. I evaluated various algorithms using four measures: (1) docket efficiency, how deep the algorithm had to look on the docket to find cases; (2) distribution diversity, how balanced prioritized cases were between judges; (3) priority timeliness, how long it took to distribute a new prioritized case; and (4) priority pending, the maximum number of prioritized cases waiting at any given time.

The challenge was that for AMA, I was modeling a novel and highly complex procedural framework with only limited data as to what might happen (collecting a preliminary evidence base was another goal of the BEAAM program, which featured extensive interviews with Veterans and their representatives to explore how they would approach making choices under AMA). It was extremely important to test the algorithm under extreme scenarios, not just how VA hoped they would play out.

AMA says, “The Board shall maintain at least two separate dockets,”[5] one for appeals that requested a hearing, and one for appeals that didn’t. The Board chose to create not two, but three dockets. As required by the statute, one docket would be for appeals that requested a hearing. A second docket would be for appeals that didn’t request a hearing, but where the Veteran had added new evidence to their case that had not been reviewed by the agency that had originally made the contested decision (i.e. the Veterans Benefits Administration for disability benefit claims). A final docket, the “Direct Review” docket, would offer Veterans the guarantee of a faster decision in exchange for not requesting a hearing or adding new evidence. When a Veteran appealed a decision to the Board, they would have to choose which docket they wanted to use. And as the dockets were maintained separately, the Board could choose how to allocate resources between them, working some dockets faster than others, while still respecting docket order within any given docket.

Veterans who already had an appeal could keep it under the old “legacy” rules. As a result, there would now be four separate dockets for the algorithm to consider: the hearings docket, the new evidence docket, the Direct Review docket, and the legacy docket.

The Board’s policy goals

The Board articulated three policy goals to inform the design of the algorithm. As is often the case, the goals are sometimes vague and contradictory. That’s what makes this fun, I guess.

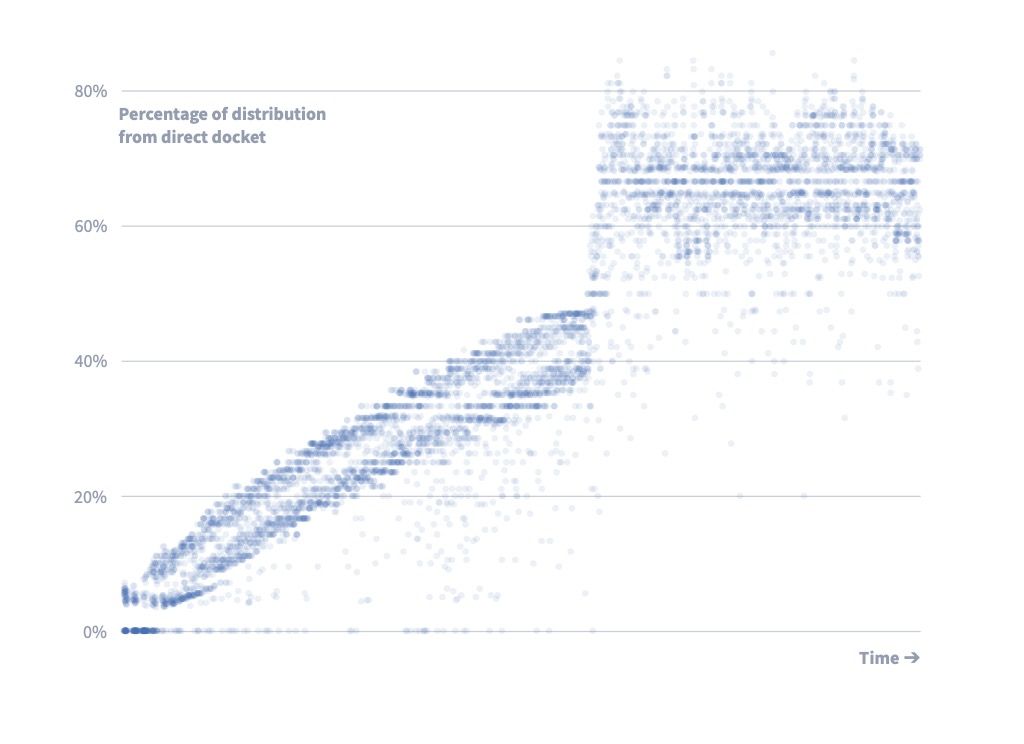

The first goal was not vague. Appeals on the Direct Review docket should be decided within one year, 365 days. I understood at the time that this was not realistic in the medium term,[6] but the Board was unwilling to acknowledge that fact. As of December 2024, appeals on the Direct Review docket take an average of 722 days to complete, down from a peak of 1,049 days in July 2024.[7] Absent any staffing reductions, it is possible that the Board will be able to reach a steady state where it consistently achieves its goal by 2026. From the perspective of algorithm design, I sought to give the Board the best shot at achieving its goal, while also ensuring the Board didn’t shoot itself in the foot if the goal turned out to be unachievable.

The second goal was that the dockets should be balanced “proportionately.” The definition of “proportionately” was left to me to interpret, but any definition was in contradiction with the other two goals. In the end, I excepted the Direct Review docket from any claim of proportionality and rearticulated this goal as “the other dockets should be balanced proportionately.”

The third goal was that the Board would prioritize completing legacy cases. The size of the legacy appeals backlog, then about 400,000 cases, was the primary reason I felt the first goal was not realistic. Under the legacy rules, Veterans have options to keep an appeal going almost indefinitely, so the Board will continue to work legacy appeals for literal decades. However, unless the Board clung too long to the 365-day goal for the Direct Review docket, I expected the Board could reach “functional zero” by 2025 or 2026, where only a small proportion of its resources were going toward the long tail of legacy appeals.

Keeping these goals in mind, let’s take a look at the AMA algorithm. Or, you know, maybe you could take a pleasant walk in the fresh air instead?

Hard mode: four dockets

As before, we start by calculating the docket margin and docket margin net of priority, only now looking at prioritized cases on any of the four dockets.

Setting aside the prioritized cases for a moment, we need to determine what proportion of non-prioritized cases should come from each of the dockets. Each docket has a weight, which is generally equal to the number of non-prioritized cases waiting.

The legacy docket’s weight is adjusted to account for cases that we know about, because the Veteran has filed a Notice of Disagreement, but which have yet to come to the Board and be docketed, because they are waiting on a Form 9. About 40% of Notices of Disagreement end up reaching the Form 9 stage, so we add a discounted count of pre-Form 9 cases to the number of docketed cases to give us the legacy docket’s weight.

classLegacyDocket# When counting the total number of appeals on the legacy docket for purposes of docket balancing, we# include NOD-stage appeals at a discount reflecting the likelihood that they will advance to a Form 9.NOD_ADJUSTMENT=0.4defweight

count(priority:false)+ nod_count *NOD_ADJUSTMENTend# ...end

We’ve now fulfilled the Board’s second goal, and calculated a set of proportions using the size of each docket. If that was our only goal, we could stop, but in response to the other two goals, we’ll make need to make two adjustments.

First, we need to fix the Direct Review docket such that cases are decided within 365 days. When a case is docketed on the Direct Review docket, Caseflow stamps it with a target decision date, 365 days after the day it was docketed. We record the target decision date for each case to enable the Board to later adjust the timeliness goal (should it prove to be infeasible), while continuing to honor the commitment that was made to Veterans when they chose the Direct Review docket. The goal is adjusted for future cases, but we continue working the cases we have within the time we promised.

From the target decision date, we can derive the distribution due date, the date that we want to start looking for a judge in order to get a decision out the door by the 365 day mark. This was initially 45 days before the target decision date, but we planned to adjust this number as we got real-world data.

We can count the number of cases where distribution has come due and divide by the docket margin net of priority to calculate the approximate proportion of non-prioritized cases that need to go to Direct Reviews in order to achieve the timeliness goal. Initially, no cases are due, and so this proportion would be zero. But the Board didn’t want to wait to start working Direct Review appeals, preferring to start working them early and notch the win of beating its timeliness goal (even if this wasn’t sustainable). As a result, I constructed a curve out for the Direct Review docket.

We start by estimating the number of Direct Reviews that we expect to be requested in a year. If we’re still within the first year of AMA, we extrapolate from the data we have. We can divide this number by the number of non-priority decisions the Board writes in a year to calculate the pacesetting Direct Review proportion, the percentage of non-priority decision capacity that would need to go to Direct Reviews in order to keep pace with what is arriving.

defpacesetting_direct_review_proportionreturn@pacesetting_direct_review_proportionif@pacesetting_direct_review_proportion

receipts_per_year = dockets[:direct_review].nonpriority_receipts_per_year

@pacesetting_direct_review_proportion= receipts_per_year.to_f / nonpriority_decisions_per_year

end

Our goal is to curve out to the pacesetting proportion over time. So we calculate the interpolated minimum Direct Review proportion, using the age of the oldest waiting Direct Review appeal relative to the current timeliness goal as an interpolation factor. We apply an adjustment to this proportion, initially 67%, to lower the number of cases that are being worked ahead of schedule.

The second adjustment that we apply to the raw proportions is that we set a floor of 10% of non-priority cases to come from the legacy docket, provided there are at least that many available. This adjustment ensures that the Board continues working the legacy appeals backlog, even as it dwindles to only a handful of cases.

A brief aside

An implicit assumption here is that the Board needed to be willing to admit when it was no longer able to meet the 365-day goal. The 80% limit gave me confidence that at least nothing would break. But if the percentage of Direct Reviews was continuously pegged to 80%, there would be scarce capacity to work anything other than Direct Reviews, and in particular, to work down the legacy appeals backlog.

To this day, VA.gov reads, “If you choose Direct Review, […] the Board’s goal is to send you a decision within 365 days (1 year).” VA continued to make that promise to Veterans even as it was issuing decisions on Direct Reviews that were more than 1,000 days old.

Again, because it’s hidden from the public, I don’t know how the Board has updated the algorithm’s parameters, or even if they’re still using it. But it’s quite apparent from publicly available data that whatever algorithm is in use, the Board has not been able to keep pace with the 365-day goal it continues to claim. Fortunately, it looks like things started to turn around in 2024 as the legacy backlog began to dry up, and it’s possible the Board will be able to meet its stated goal within the next couple years. If its staffing levels aren’t cut.

Hearings make this even harder

Okay, one last complication. Under AMA, cases on the hearings docket get distributed to judges as soon as they are ready, generally after the hearing has occurred, been transcribed, and the evidentiary period (the time after the hearing in which the Veteran can add new evidence to their case) has expired or been waived. The Board’s term for this is “one-touch hearings,” which is in contrast to legacy hearings, which could take place months or even years before the case was decided. As a result, the number of cases that get worked on the docket is not decided when cases are distributed, but rather when we determine how many AMA hearings to hold.

Fortunately, Caseflow is also responsible for scheduling hearings. Every quarter, Caseflow Hearing Schedule asks Caseflow Queue (where the algorithm lives) to tell it the number of AMA hearings it should schedule. Caseflow calculates the docket proportions, as above, and multiplies the hearings docket proportion by the number of non-prioritized decisions it plans to issue that quarter.

One complication of this number is that a Veteran could withdraw their hearing request. Due to a legal technicality, however, their appeal would remain on the hearings docket. This means that Caseflow Hearing Schedule needs to look to whether the hearing request had been withdrawn. If so, it marks the case as ready for a decision; if not, it schedules a hearing.

Under AMA, cases with hearings are not required to be decided by the same judge who had held the hearing, as they were under the legacy rules. However, it remains better for everyone involved if the same judge decides the case, if possible, so the algorithm continues to mostly work the same, which I termed affinity. The only difference between affinity and the old rules is that if a judge retires or takes a leave of absence, Caseflow treats the cases they heard as gen pop, available to be assigned to anyone, instead of requiring another hearing.

At long last, let’s automatically distribute some cases

Okay, so now we know the proportion of the Board’s decisions that should be allocated to each docket. We’ve helped Caseflow Hearing Schedule hold the right number of hearings some months ago. Now a judge comes along and asks for a new batch of cases. Let’s help them out, shall we?

As before, we calculate the priority target and docket margin net of priority. The only difference is that we now need to look at the number of prioritized appeals on any of the four dockets. We’ll also calculate how deep we can look on the legacy docket specifically, the legacy docket range by multiplying the docket margin net of priority by the legacy docket proportion.

deflegacy_docket_range(docket_margin_net_of_priority * docket_proportions[:legacy]).round

end

We can start distributing appeals by looking at cases that are either tied to the judge (legacy docket) or have affinity for the judge (hearings docket). And of course, prioritized cases go first.

# Distribute priority appeals that are tied to judges (not genpop).

distribute_appeals(:legacy,limit:@rem,priority:true,genpop:"not_genpop")